If you’re thinking about buying a home, you’ve probably heard plenty of advice, from family, friends, and the internet. While most of it comes from good intentions, a lot of it can be misleading and even a little scary. These myths often spook first-time buyers out of taking the next step. Knowing what’s fact and what’s fiction can help you start your homeownership journey with confidence. Here are five common home buying myths that don’t need to scare you off:

Myth 1: You need to put 20% down.

Many first-time home buyers hear that they need a down payment of at least 20% to purchase a home. This advice has been around for decades, but it scares some individuals away from saving for a house because they feel like they’ll never be able to save up a down payment. In some markets, a 20% down payment on a modest house could be $100,000 or even more.

The Truth

You don’t need anywhere close to a 20% down payment to purchase a home. This misconception most likely comes from the fact that you need at least 20% equity in your house to avoid paying private mortgage insurance. Making a larger down payment will also reduce your monthly mortgage payment and reduce your risk of going underwater on the loan.

However, buyers can be approved for a mortgage with a down payment of as little as 3.5% on an FHA loan or 3% on a conventional loan. You don’t need to save for decades to afford your first home. Making a smaller down payment has its downsides, but it can also make homeownership accessible to you earlier, which gives you more years to build equity in the property.

Myth 2: Your credit score must be perfect.

Prospective homeowners hear a wide variety of rumors about what their financial status needs to be in order to buy a house. Here are some of the most common credit-related misconceptions:

- Your credit score should be over 700.

- Student loans will disqualify you from mortgage approval.

- Credit card debt will disqualify you from mortgage approval.

- You can’t get a mortgage if you have derogatory marks on your credit report.

The Truth

The better your credit score and overall financial health, the easier it will be for you to buy a home. You don’t need perfect credit to be approved for a mortgage, though.

You can be approved for an FHA loan with a credit score of 580. If you make a 10% down payment, you can even get an FHA loan with a score as low as 500. Conventional mortgage lenders usually require a credit score of at least 620.

Plenty of home buyers have student loans, car payments, or other forms of debt when they apply for mortgages. The general rule of thumb is to have a debt-to-income ratio of less than 36%, but you may be able to get a mortgage with a debt-to-income ratio as high as 50%.

It’s never advisable to rush into homeownership if you’re not financially ready. You should feel confident that you can make all your monthly payments and have money leftover to save for emergencies. However, you don’t need perfect credit to apply for a mortgage.

Myth 3: You should wait for the market to change.

Prospective home buyers often hear that now isn’t the right time to buy a house and that they should wait for the market conditions to improve. If interest rates are high, buyers should wait a year for rates to drop. If the housing supply is low, they should wait until the market is more active.

The Truth

If you wait for the perfect conditions to buy a house, you might be waiting forever. There will always be pros and cons to buying at any time, and it’s impossible to predict how the market will change.

Instead of trying to time your home purchase based on the market conditions, focus on your own personal preparedness. You should know when it’s time for you to enter the real estate market based on your financial circumstances, your career, and your long-term plans. If you can afford a mortgage, know where you want to live, and feel excited at the idea of homeownership, it’s time to consult with a real estate agent.

Myth 4: Spring and summer are the best seasons to buy a house.

Spring and summer are the most active times of year for the real estate market. This leads some buyers to believe that they should only look for homes during these seasons. You might feel like you have to pause your home search during the winter so that you can hold out for the properties that will come on the market in the spring.

The Truth

While it’s true that spring into early summer is the most popular time of year for home buyers, that doesn’t necessarily mean it’s the best time for you to buy a house. Homeownership is a personal journey, and your own wants and needs are more important than market trends.

In fact, there can even be benefits to buying a house in the off-season. You’ll be competing with fewer buyers, so you don’t have to rush into making offers. Sellers are often more motivated in the fall and winter, too, so you have more negotiating power.

Myth 5: You have to stay put forever.

Buying a house is a much bigger commitment than signing a rental agreement, so some people will tell you only to buy a home if you’re sure you’re going to stay in the area forever. If you have any uncertainty about your future plans, you might be scared to pursue homeownership.

The Truth

You don’t need to stay in a house that you buy forever. Most real estate professionals will advise you to stay in a home for at least five years to ensure you get a return on your investment. As long as you can imagine yourself living in the house for at least five years, you should consider buying it.

Very few people know exactly where they want to spend the rest of their lives, and unexpected life changes happen all the time. While you should have a general idea of what you want the next five to 10 years to look like when you buy a home, you shouldn’t feel like you’re going to be stuck in one house forever.

Buying a home can feel intimidating, but don’t let these myths scare you off. With the right guidance and preparation, you can take that next step toward homeownership with confidence. Contact your favorite Romeo Team Realty agent today to get started!

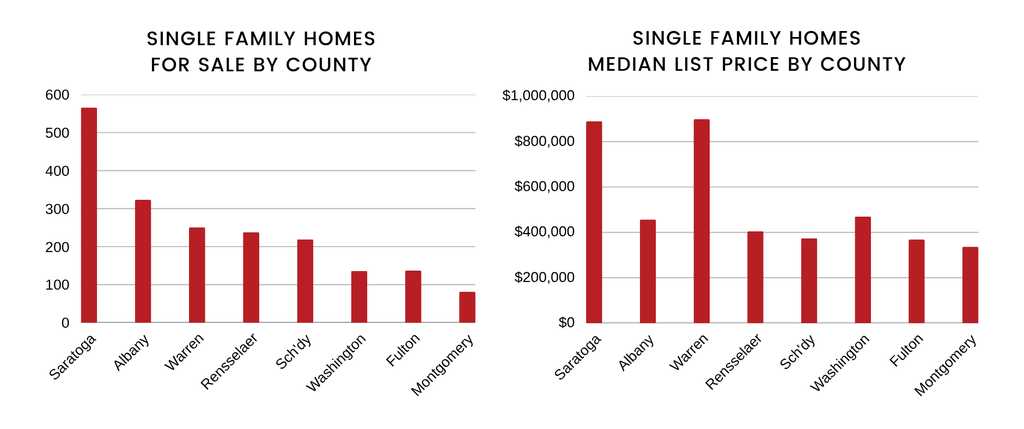

Market Updates

In September ‘25, homes spent a median of 9 days on market, marking the 3rd consecutive month of gradual increase since June. The average sale price rose to $408,097, up 4.2% from $391,657 in September ‘24. Inventory continues to rise slowly but remains limited, with an absorption rate of just 2.91 months—the time it would take to sell all current listings if no new homes came on the market and sales continued at the same pace.

Homes that are priced appropriately and presented as move-in ready continue to sell quickly and often receive multiple offers, while properties listed higher or requiring significant updates are experiencing longer market times. As more homes come on the market, sellers face increased competition, and we’re entering a slower seasonal period—one that can bring both opportunities and challenges for buyers and sellers alike. Source: Global MLS 10.16.2025